Ricochet is the best place on the internet to discuss the issues of the day, either through commenting on posts or writing your own for our active and dynamic community in a fully moderated environment. In addition, the Ricochet Audio Network offers over 50 original podcasts with new episodes released every day.

Two Things to Remember About Health Care Policy

Two Things to Remember About Health Care Policy

When trying to formulate a logical, humane health care system, the key is to start from this fundamental understanding: In our wealthy Western countries, we’re not going to let people die in the streets because they can’t afford readily available health care treatments.

When trying to formulate a logical, humane health care system, the key is to start from this fundamental understanding: In our wealthy Western countries, we’re not going to let people die in the streets because they can’t afford readily available health care treatments.

Since everyone knows we aren’t going to turn people away from emergency rooms, a completely free market won’t work. The free rider problem is insurmountable. People can and will choose not to participate in the market until they become sick, and they will then rely on the good will of society to care for them. So the government will be involved in the health care delivery system in some way. Given the free rider problem, it should do so realistically: It should help people at the bottom while keeping government distortion of the market to a minimum.

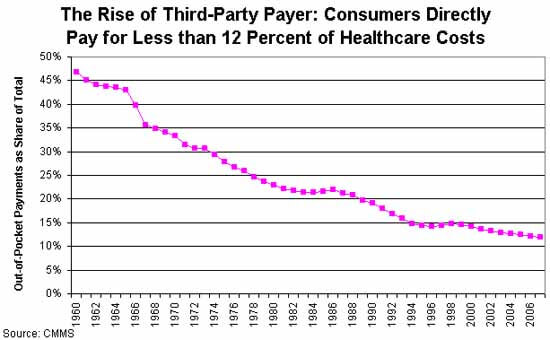

The next thing to consider is the big question: Why is health care so expensive? There’s widespread agreement that third-party payment through insurers is the main problem. There’s no cost control, because neither doctors nor their patients have any incentive to control costs. The only way to gain control over costs is to increase bureaucratic oversight – which adds to the cost.

The next thing to consider is the big question: Why is health care so expensive? There’s widespread agreement that third-party payment through insurers is the main problem. There’s no cost control, because neither doctors nor their patients have any incentive to control costs. The only way to gain control over costs is to increase bureaucratic oversight – which adds to the cost.

Given these two broad parameters, it seems to me that a free-market health care system (or one that’s as free as possible given the first constraint) should begin with universal, single-payer, catastrophic coverage only insurance. That insurance should be very limited in scope to minimize the third-party payer problem.

In a universal catastrophic insurance system, the government would pick up your health care costs, but only if your health care problems reached a threshold such that they were a very significant hardship. This would prevent casual abuse of the system, and it would keep government costs low by eliminating the coverage of routine medical expenses. So: no coverage for routine exams, birth control, small procedures – the things that make up a huge percentage of costs, but should never be paid via an inefficient insurance system. And nothing at all should be covered until you hit your deductible.

To make this palatable to progressives, you can raise the deductible in tandem with income. So a person who makes $20,000 a year might only have to pay for health care until the bills hit $2,000 in a year; a person making $200,000 might be responsible for the first $20,000. Bill Gates might be responsible for the first billion. The numbers and time limits could be negotiated. The important point is that you are responsible for your own health care, but if faced with a health emergency that would bankrupt you, the government will step in. A progressive scheme like this would push more health care into the free market, rather than increasing the scope of government.

Now, would this mean that people would have to pay the deductible out of pocket? Of course not. Employers can offer gap insurance, as can private insurers, on an open market. Gap insurance is much less expensive than full insurance because the insurer’s risk is capped. Pre-existing conditions only cost them up to the cap, so the premium for those would be lower. Because the insurer’s liability is lower for lower-income people (because the cap is lower), insurance would be less expensive for the poor.

People who wish to self-insure could open a HSA and save, say, five times their annual deductible, completely tax-free. This would encourage more people to self-insure to cover the gap, and keep even more of the market out of the third-party payer economy.

This plan would be similar to the health care system in Singapore, a country that spends far less than the US as a proportion of GDP on healthcare, and arguably provides better health care. Singapore also adds a mandatory health savings account, Medisave, to ensure people save enough to pay for the deductible.

Comments?

Published in Domestic Policy, General

Example of such societies that still exist in some degree are the Freemasons and the individual farm bureaus.

Reading Wikipedia’s entry on health sharing ministries, it seems they’re unlike the old mutual aid organizations in that they don’t “use actuaries” or “accept risk”. The old mutual aid organizations began while risk-assessment was still in its infancy, true, but they got into actuarial work in order to manage their benefits better. Many women (men, too, I’m sure, but there were a lot of women) became actuaries, and contributed to the advancement of actuarial science, because of their long involvement in mutual-aid societies.

It strikes me as implausible that health sharing ministries would literally avoid all actuarial work. How else would they husband their benefits responsibly, to best serve their members? But perhaps they have to avoid official actuarial work in order to remain exempt from insurance regulations.