Ricochet is the best place on the internet to discuss the issues of the day, either through commenting on posts or writing your own for our active and dynamic community in a fully moderated environment. In addition, the Ricochet Audio Network offers over 50 original podcasts with new episodes released every day.

Is America’s Nearly 150-Year Streak of Steady Growth at an End?

Is America’s Nearly 150-Year Streak of Steady Growth at an End?

Call it the New Normal or Great Stagnation, but there’s plenty of concern that America’s weak 2000s growth rate — before and after the Great Recession and Financial Crisis — is a harbinger of anemic growth to come. And GDP has indeed been weak, just 1.9% annually since 1999 vs. 3.6% from 1948-99.

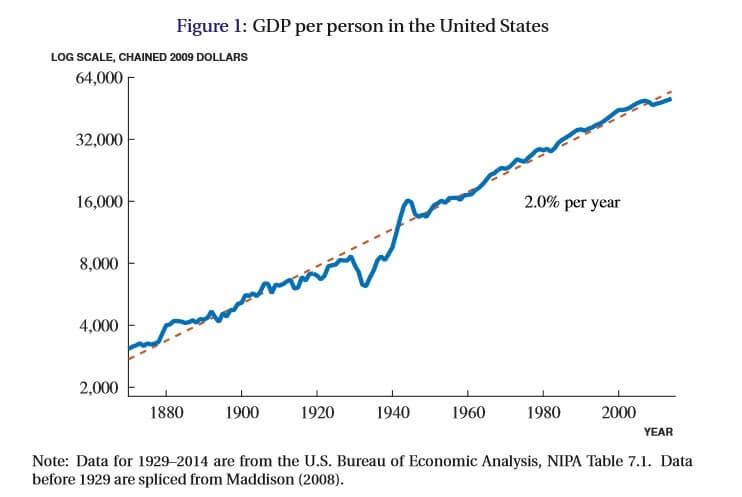

Yet if you look at GDP growth on a per capita basis and compare it to America’s longer-term growth trend, it doesn’t look nearly so dire, as NYU economist William Easterly points in a tweet — “That horribly traumatic Growth Slowdown in the US may not actually exist” — highlighting this chart from Stanford economist Charles Jones:

Jones from his paper, “The Facts of Economic Growth”:

For nearly 150 years, GDP per person in the U.S. economy has grown at a remarkably steady average rate of around 2 percent per year. Starting at around $3,000 in 1870, per capita GDP rose to more than $50,000 by 2014, a nearly 17-fold increase. Beyond the large, sustained growth in living standards, several other features of this graph stand out. One is the significant decline in income associated with the Great Depression. However, to me this decline stands out most for how anomalous it is. Many of the other recessions barely make an impression on the eye: over long periods of time, economic growth swamps economic fluctuations. Moreover, despite the singular severity of the Great Depression — GDP per person fell by nearly 20 percent in just four years — it is equally remarkable that the Great Depression was temporary. By 1939, the economy is already passing its previous peak and the macroeconomic story a decade later is once again one of sustained, almost relentless, economic growth.

But is 2%-ish what we can expect in the future? Given (a) demographic trends affecting the labor force and (b) the assumption that productivity will maybe return to its post-1960s average but no better, what might we expect? Here is John Fernald, chief economist of the SF Fed, in a paper out last week:

What is the sustainable pace of GDP growth in the United States? A plausible point forecast is that GDP per capita will rise well under 1 percent per year in the longer run, with overall GDP growth of a little over 1-1/2 percent. The main drivers of slow growth are educational attainment and demographics. First, rising educational attainment will add less to productivity growth than it did historically. Second, because of the aging (and retirements) of baby boomers, employment will rise more slowly than population (which, in turn, is projected to rise slowly relative to history). This modest growth forecast assumes that productivity growth is relatively “normal,” if modest—in line with its pace for most of the period since 1973. … Once the economy recovers fully from cyclical dynamics associated with the Great Recession, GDP growth is likely to be well below historical norms, plausibly in the range of 1½ to 1¾ percent per year. Looking, say, 7 to 10 years out, my preferred point estimate is 1.6 percent growth in GDP per year, with per capita growth of under 0.9 percent. The reason for the slow pace is not primarily productivity, in that we’ve previously seen long periods (such as 1973-95) with modest productivity growth. Rather, it’s the combination of modest productivity growth with demographics.

How might per capita GDP growth that low feel (assuming past patterns of income distribution hold)? Well, during the Not-So-Great Recovery since 2009, per capita GDP growth has been about 1.4%. So, yeah. Better try and boost productivity. Indeed, Fernald cites as an “upside risk” that we “see another burst of information-technology-induced productivity growth similar to what we saw from 1995 to 2004.”

Also: “Raising growth above this modest pace depends primarily on whether the private sector can find new and improved ways of doing business.”

Innovation!

Published in Economics

Give us enough time to massage and revise the figures we will make the Obama years look like Nirvana.

Log graphs can make practically anything look linear.

I have been saying this for a while. We are never returning to 4% real GDP growth because our population is no longer growing fast enough. GDP per capita is the right way of measuring the economy when you care about the effects on people in that economy.

I think this trend in GDP growth per capita will continue, automation technologies will always continue. The area where GDP per capita may see headwinds is in the shift from physical goods and services to virtual goods and services, which have such low marginal cost of production that the price can often be zero to the consumer.

JamesP,

Sorry but this is garbage. Lower the corporate tax rate. Pull back the absurd regulations on energy and the environment. Stop artificially promoting women & minorities and force them to compete for jobs. Stop the ACA from raising the price of Health Insurance. Stop the FDA from creating crony monopolies and inflating the price of drugs. Ensure freedom of speech & research on university campuses. Stop imagining that there is some magical Global Governance that will create world stability and get back to a real foreign policy.

America will slam forward and revert to the world’s most powerful economy pronto. This ain’t rocket science but we could start a Manned Mars Mission tomorrow too.

Regards,

Jim

As James Gawron says above, “Garbage.” If you tracked government intervention in business over the same time frame as the charts above, I suspect you would see a direct inverse correlation between increased intervention and decreased economic growth. I wonder if any economist has actually done a chart like that.

As for “educational attainment” adding less to productivity, yes, that makes sense when you consider that the education system is producing a less and less useful product. Degree in “Women’s Studies” anyone?

His comment about aging above doesn’t parse. Are baby boomers retiring? If so, their jobs will become available. If they are not retiring, then the jobs are filled and employment is unaffected.

I agree with Mr. Walker 100% – the vast majority of “growth” in the new century has been in things like regulatory compliance, parking lot surveillance and other security guards and services, drug and alcohol rehab spas, babysitting the homebound and mentally challenged through Medicaid companions, “free” scooters, etc. – items that would not be purchased with marginal dollars in a free marketplace or that don’t feel like growth to the average citizen. And I also have to argue with Z from MT’s contention about the population growth rate. The big problem in the future will be to structure ergonomically more employment for lackadaisical, entitled workers rather than deal with shortages. Immigration policy will not help us out; we are consciously and deliberately following a policy to lower our human capital by putting our thumb in the eye of those that could contribute to growth from Asia or Europe in order to bring in those that will be wards of the social services industrial complex for the next four generations; primarily now from Central America or Somalia, in the near future from the rest of Africa and Mid-East.

I don’t think there will be any shortages of workers. There is going to be a huge excess of workers as automation takes over. In the future a small handful of people (<10% of the population) will be responsible for 80% of GDP. The real problem will be that a huge sector of the economy will be in virtual goods (cool ninja swords for your World of Warcraft Avatar, that you spend 30 hours a week playing). Even with artificial scarcity like with bitcoin these virtual goods have near zero marginal cost of production and very low prices, so a large growing sector of the economy will not show up in GDP figures.

We have been experiencing a fake economy for years, supported by historically unprecedented levels of debt accumulation and money printing. When it finally implodes we will realize recent growth wasn’t real anyway, so there isn’t much point arguing over whether phony growth is 1.5% or 2%.

It would be enlightening, à la comment #6 by anonymous, were someone interested in actually portraying the truth able to calculate the contribution of bloated government to these GDP ‘measurements.’. Given the widespread expertise in massaging and tweaking data so as to create false perceptions, surely it is possible to distill a more accurate picture of annual GDP change over time. Is GDP even the best metric of growth over time? I ask that question in all honesty, I do not know.

What? I look at that graph and I see the longest period beneath the 2% trend line since the Great Depression, and it seems to be trending lower. Am I reading it wrong?